Paper Title: Deep learning-driven regime switching models for capturing structural breaks and volatility clustering in financial time series

Author: Junyu Wang

Corresponding Author: Junyu Wang (s4816977@uq.edu.au)/Australia

Abstract

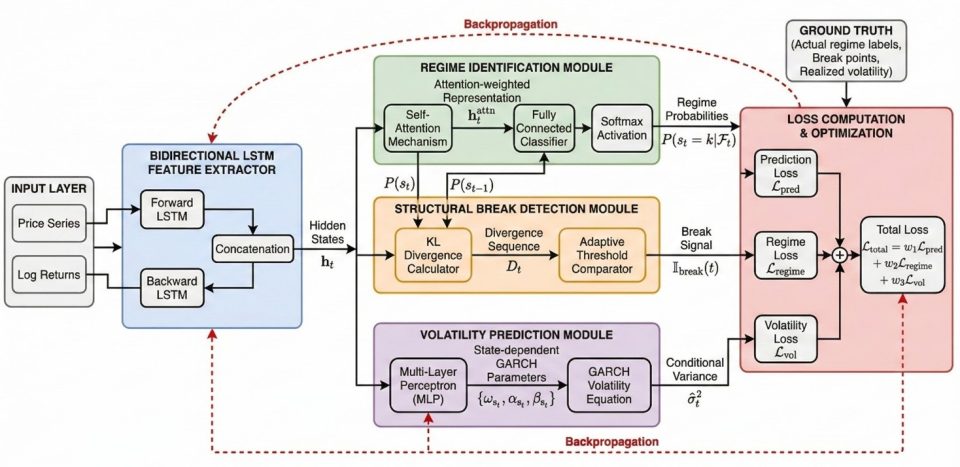

The mechanism of switching and the identification of structural breakpoints in financial markets across different macro environments have long been core challenges in asset pricing and risk management. Traditional parametric models suffer from insufficient flexibility to capture nonlinear dynamic processes. This study proposes a regime-switching model driven by deep learning. By integrating a bidirectional long short-term memory network with the probabilistic inference framework of the Markov transformation process, a unified optimization framework for structural break identification, market regime classification, and volatility clustering modeling is constructed, in which the attention mechanism dynamically focuses on key historical information to enable mechanism identification. A multi-layer perceptron generates state-dependent GARCH parameters to adaptively capture the characteristics of heterogeneous fluctuations, and adaptive threshold monitoring based on KL divergence enables quantitative identification of structural breaks. Experiments show that the model achieves significant performance advantages over traditional methods in structural break detection, mechanism transition identification, and volatility prediction. The cross-market generalization ability and robustness analysis verify the model’s applicability across different asset classes and time horizons. The posterior probability distribution of the model’s state output can support asset allocation decisions, and the breakpoint identification mechanism provides quantitative early-warning indicators for regulators. It has important practical value in scenarios such as portfolio management, market timing strategies, and systemic risk prevention.

Keywords

Deep learning, Regime switching model, Structural break, Volatility clustering, Financial time series

Cite:

Wang, J. (2026). Deep learning-driven regime switching models for capturing structural breaks and volatility clustering in financial time series . Future Technology, 5(2), 268–280. Retrieved from https://fupubco.com/futech/article/view/815