Paper Title: Deep Learning-based anomaly detection in stock markets and business decision support

Authors: Changjiang Dai

Corresponding Author: Changjiang Dai (daichangjiang008@163.com)/ Malaysia

Abstract

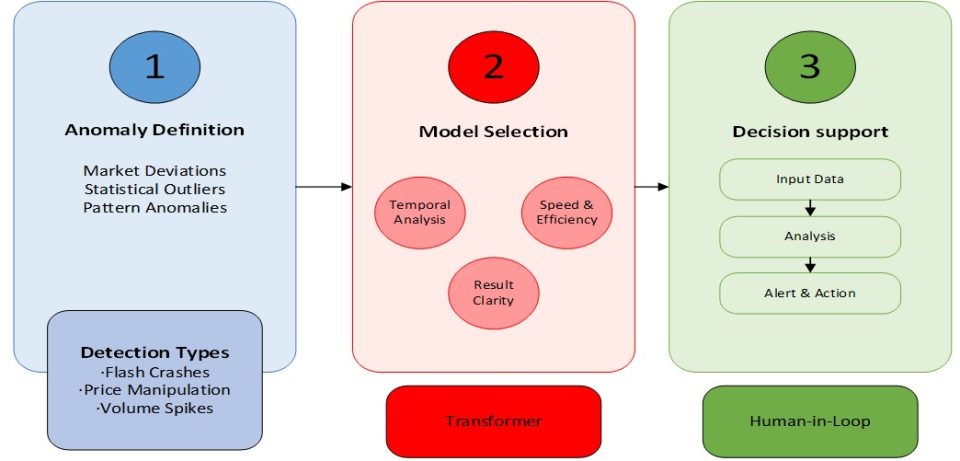

The increasing complexity and volatility of modern financial markets necessitate advanced anomaly detection systems that can identify irregular patterns, which may signal market manipulation, systemic risks, or emerging crises. This research presents a comprehensive deep learning framework for real-time anomaly detection in stock markets, integrated with business decision support systems to enhance risk management and regulatory compliance. We propose and evaluate four distinct deep learning architectures: LSTM-Autoencoder, Variational Autoencoder (VAE), Transformer-based models, and an ensemble approach, utilizing high-frequency trading data from major stock exchanges spanning 2019-2024. Our methodology incorporates multi-dimensional feature engineering, including technical indicators, market microstructure variables, and sentiment analysis, processed through advanced normalization techniques. The experimental results demonstrate that the Transformer-based ensemble model achieves superior performance with an F1-score of 0.89 and AUC of 0.94, representing a 43.5% improvement over traditional methods (F1=0.62 for ARIMA-GARCH) and 17% improvement over standalone machine learning approaches (F1=0.76 for XGBoost). The system successfully detected 92% of major market anomalies with a 15-minute average early warning time while maintaining a false positive rate below 3%. Furthermore, the integration with decision support systems yielded a 34% improvement in risk-adjusted returns for test portfolios, reducing decision-making time by 67.3% (from 98s to 32s) and achieving cost savings of $35.2M monthly across deployed institutions. This research contributes to financial technology by bridging the gap between advanced deep learning techniques and practical business applications, offering a scalable solution for market surveillance and risk management in increasingly complex financial ecosystems.

Keywords

Deep learning, Anomaly detection, Stock market, Transformer models, Business decision support, Real-time detection

Cite:

Dai, C. (2025). Deep Learning-based anomaly detection in stock markets and business decision support. Future Technology, 4(4), 296–310. Retrieved from https://fupubco.com/futech/article/view/410